What You Need to Know about Home Appraisals

So what exactly IS an appraisal?

A good definition is an objective way to estimate the fair market value of a property.

Understanding value is important for all parties involved in the mortgage process.

Because this value is essential to both the homeowner/buyer and the lender, appraisals are performed by a licensed, objective third party known as an appraiser.

When this professional is determining a value estimate, they will consider the home’s location, age, square footage, amenities, and structural condition, as well as recent comparable property sales.

All mortgage lenders require appraisals whether the loan is for a home purchase or refinance, verifying that the price you’re willing to pay is on par with the actual value of the home.

How does the appraisal process work?

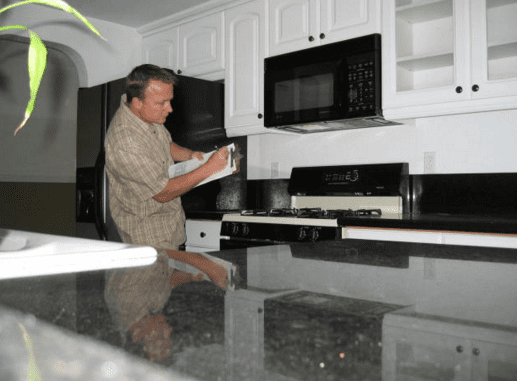

Once your loan application is taken, an appraisal is ordered by the mortgage company through an AMC or Appraisal Management Company. The AMC contacts a local appraiser that is familiar with your area to come inspect and write the report.

The report is created with attention to all relevant documentation about the home, including the deed, survey, purchase agreement, and other pertinent information.

There are three basic steps to residential appraisals.

- On-site evaluation. The appraiser inspects the property and notes amenities, structural attributes, the number of bedrooms and bathrooms, the square footage and other characteristics. This assessment should not be confused with a home inspection, in which the structural and functional condition of the home are evaluated.

- Market research. Recent comparable sales, or comps, will be evaluated to assess the market value of real estate in your area. This base figure is then adjusted based on the differences between your property and the attributes of other sales (property features, finished vs. unfinished space, exterior features such as garages, pool/spas etc).

- Appraisal report. The appraiser issues a final assessment estimating the value of the property. You will receive a copy of the appraisal report because of the Equal Credit Opportunity Act.

Why are appraisals necessary?

To keep it simple, appraisals protect both the lender and the borrower from overpaying. Lenders are protected by appraisals, as the home serves as collateral for the mortgage and the value is compared to the loan amount.

Sometimes a buyer makes an offer that an appraisal reveals to be below market value, that buyer could then back out of the sale through an appraisal contingency.

An appraisal contingency is a commonly used provision that real estate agents build into a purchase offer, and it protects homebuyers from being forced to accept reduced equity in the property.

Listing price vs. appraisal value

Listing prices are not generally determined based on an appraisal, but instead by using a Comparative Market Analysis (CMA). A CMA is performed by a real estate agent to arrive at a listing price.

While experienced real estate agents can arrive at a listing price that is often very close to the value estimated by an appraisal, mortgage companies do not accept CMAs as proof of value.

An experienced loan officer like Jackie, can also provide public record information of recent sales comparables to come to an estimate of value before an expensive appraisal is ordered.

Who pays for the property appraisal?

Although lenders order the appraisal through the appraisal management company, the buyer pays for it after they have confirmed their intent to proceed with a loan transaction.

How Much is an Appraisal?

Typical appraisal can run $450-$550 for a conventional or FHA / VA loan. Jumbo loan appraisals, multiple units or unusual property types can run $600 or higher depending and the appraisal company and how much work is involved.